Most founders treat startup health insurance the way they treat dental cleanings—important, but easy to put off until something forces the issue. Then a key engineering candidate asks about your health plan, a new hire’s spouse has a chronic condition, or you cross an employee headcount that triggers federal compliance rules. Suddenly, “we’ll figure it out later” isn’t a strategy anymore.

For another helpful perspective, this Startup Health Insurance highlights practical trade-offs for buyers. This guide is built for founders and early operators running teams of roughly 5 to 75 people, especially venture- and growth-stage startups. Below, we’ll walk through how to build your first benefits program from scratch—what to offer, how to fund it, and how a modern, tech-forward approach lets a lean startup launch competitive coverage fast, the way a much larger company would.

Startup Health Insurance: Why Benefits Matter Earlier Than You Think

When you’re conserving runway, it’s tempting to treat benefits as a luxury you’ll add after the next funding round. However, for most growth-stage startups, the right benefits package pays for itself in three ways.

Recruiting. Top talent compares offers, and compensation isn’t just salary anymore. For example, when two startups are bidding for the same senior hire, the one with real health coverage, retirement matching, and disability protection usually wins. Moreover, strong benefits signal that you’re a serious company building something durable—not a side project.

Let's customize your 2026 benefits strategy.

Complete our quick form for a free consultation, call (800)779-4090 today, or email service@waughagency.com to get started.

Retention. Replacing an employee can cost a significant fraction of their annual salary. Therefore, a solid health plan and supporting benefits reduce the friction that pushes people to look elsewhere, especially employees with families who need stability.

Compliance. This is the one founders miss. As you grow, federal and state rules switch on automatically. Once you hit 50 full-time-equivalent employees, the Affordable Care Act’s employer mandate applies, requiring you to offer affordable, qualifying coverage or face penalties. In addition, other thresholds bring COBRA, ERISA reporting, and nondiscrimination requirements. You can review the official rules through the IRS employer shared responsibility provisions. Consequently, building your program thoughtfully now means you’re not scrambling—or paying fines—later.

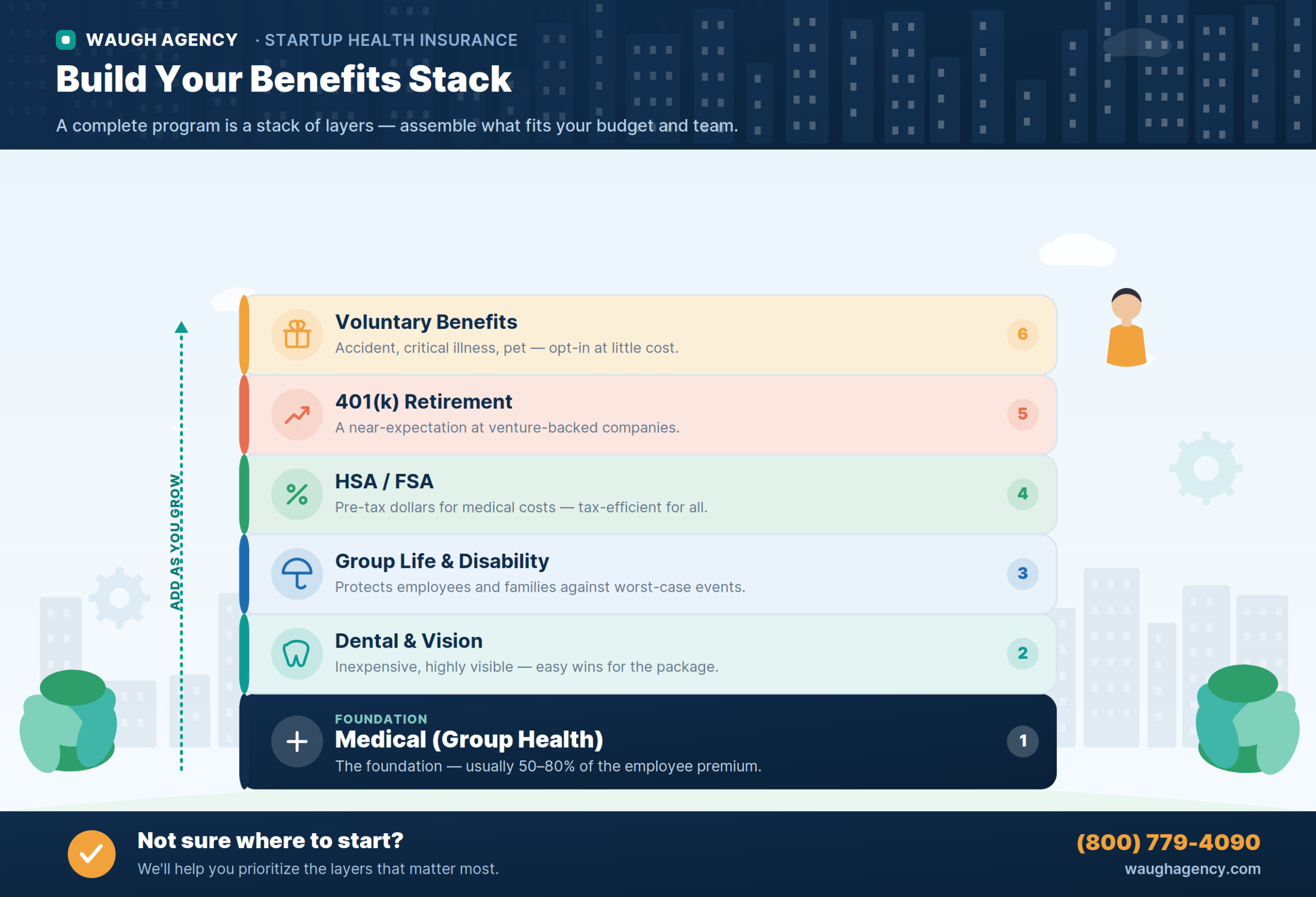

The Building Blocks of a Startup Health Insurance Program

A complete program is more than just medical coverage. Instead, think of it as a stack of layers you can assemble based on budget and team needs.

Medical (Group Health)

This is the foundation. Group health coverage is what candidates ask about first, and it’s typically the largest line item. Notably, most startups split premiums with employees, often covering 50–80% of the employee’s portion.

Complete our quick form for a free consultation, call (800)779-4090 today, or email service@waughagency.com to get started.

Dental and Vision

These options are relatively inexpensive and highly visible to employees. As a result, they are easy wins that round out a package without straining your budget.

Group Life and Disability

Group term life and short- and long-term disability protect your employees and their families against worst-case scenarios. Basic group life coverage is affordable and broadly appreciated. You can learn more about structuring this layer on our group life insurance page.

HSA and FSA

Health Savings Accounts (paired with high-deductible plans) and Flexible Spending Accounts let employees set aside pre-tax dollars for medical costs. Furthermore, they’re tax-efficient for both the company and your team.

Retirement

A 401(k)—with or without an employer match—has become a near-expectation at venture-backed companies. Fortunately, modern providers make plan administration far simpler than it used to be.

Voluntary Benefits

Accident, critical illness, hospital indemnity, pet insurance, and similar offerings let employees opt into extra coverage at little or no cost to you. In short, they add perceived value and flexibility.

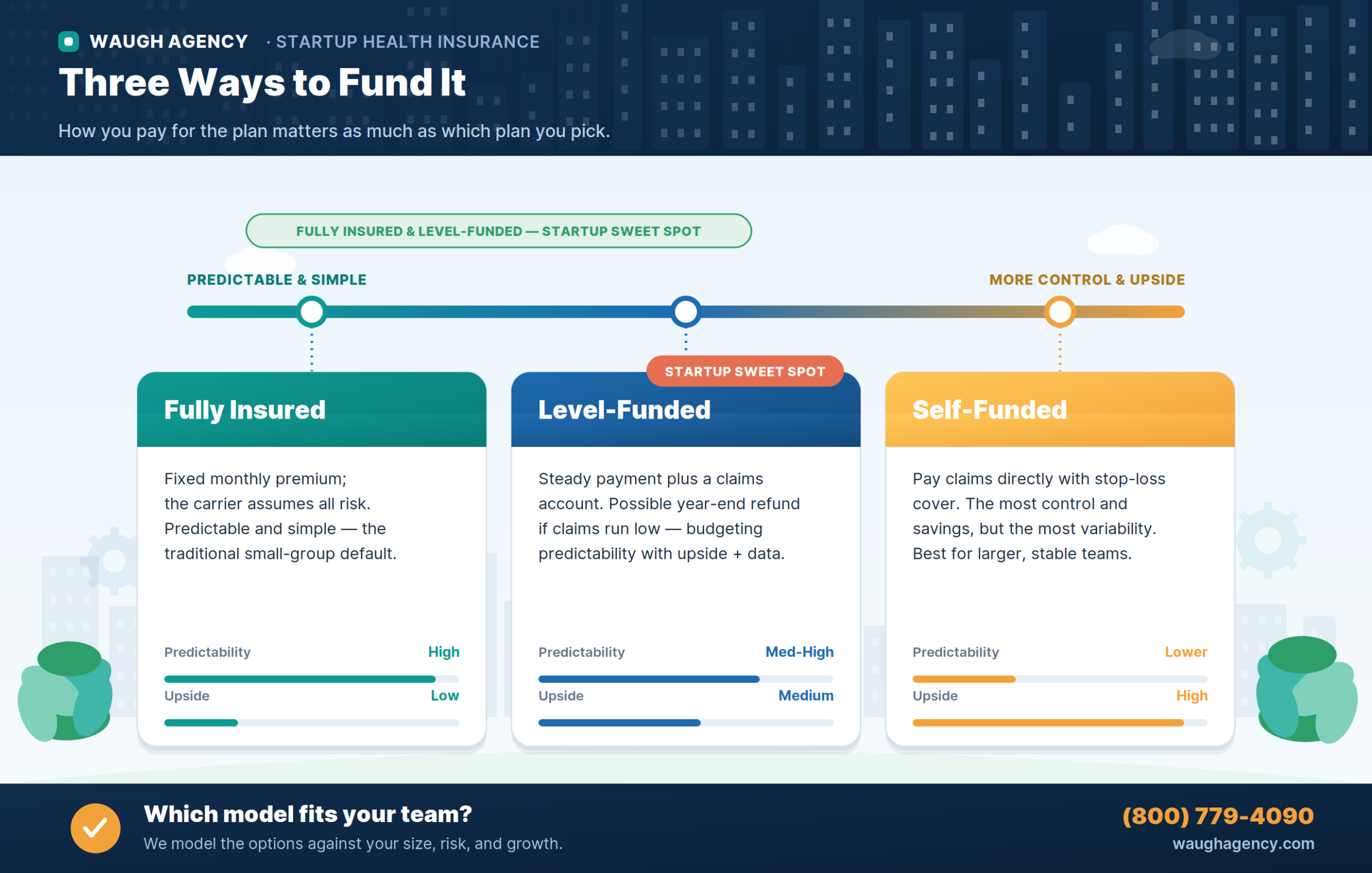

Funding Choices, Explained Simply

How you pay for your health plan matters as much as which plan you pick. Generally, there are three main models, and the right one depends on your size, risk tolerance, and growth trajectory.

Fully Insured

You pay a fixed monthly premium to an insurance carrier, and they assume all the claims risk. It’s predictable and simple—the traditional default for small groups. On the other hand, the tradeoff is that you don’t share in any savings if your team stays healthy.

Level-Funded

This is a hybrid model that’s increasingly popular with startups. You pay a steady monthly amount, but part of it funds a claims account. If your team’s claims come in low, then you can receive a refund at year-end. As a bonus, you get budgeting predictability with upside potential, plus access to claims data that fully insured plans rarely share.

Self-Funded

You pay claims directly (usually with stop-loss insurance to cap catastrophic exposure). This offers the most control and potential savings, but also the most variability. Typically, it makes sense for larger, more stable teams, rather than a brand-new five-person company. However, there are some new programs that allow much smaller employers even down to below 10 on a health plan to take advantage of self funded health insurance. For a deeper look, see our guide on self-funded health insurance and AI for small business.

For most early-stage startups, fully insured or level-funded is the sweet spot. As you scale, we help you re-evaluate.

Complete our quick form for a free consultation, call (800)779-4090 today, or email service@waughagency.com to get started.

The Tech Layer Behind Modern Startup Health Insurance

Here’s where a modern approach changes everything. A 20-person startup doesn’t have a benefits team—often it doesn’t have an HR person at all. Traditionally, that meant either drowning the founder in paperwork or paying for headcount you can’t justify yet.

Our tech-forward, AI-assisted process replaces that missing infrastructure. For instance, online enrollment lets employees pick plans from their phones in minutes. Meanwhile, the Employee Navigator platform centralizes enrollment, document storage, and ongoing administration in one place—syncing with payroll and carriers so you’re not re-keying data or chasing forms.

Additionally, automated compliance tracking flags ACA thresholds, manages required notices, and keeps you ahead of reporting deadlines. And data-driven plan analysis means we don’t just hand you a quote—we model options against your team’s actual usage and budget, then revisit them each year. Ultimately, it’s the kind of sophisticated benefits operation a Fortune 500 runs, scaled down and made affordable for a startup. Explore some of what we use on our tools page.

Ready to see what your program could look like? Book a free startup benefits consult and we’ll map out your options—no obligation, no jargon.